Become a Partner click here

The Duvanta ecosystem creates value for every stakeholder in mortgage distribution

Drive worry-free. Save time, close faster.

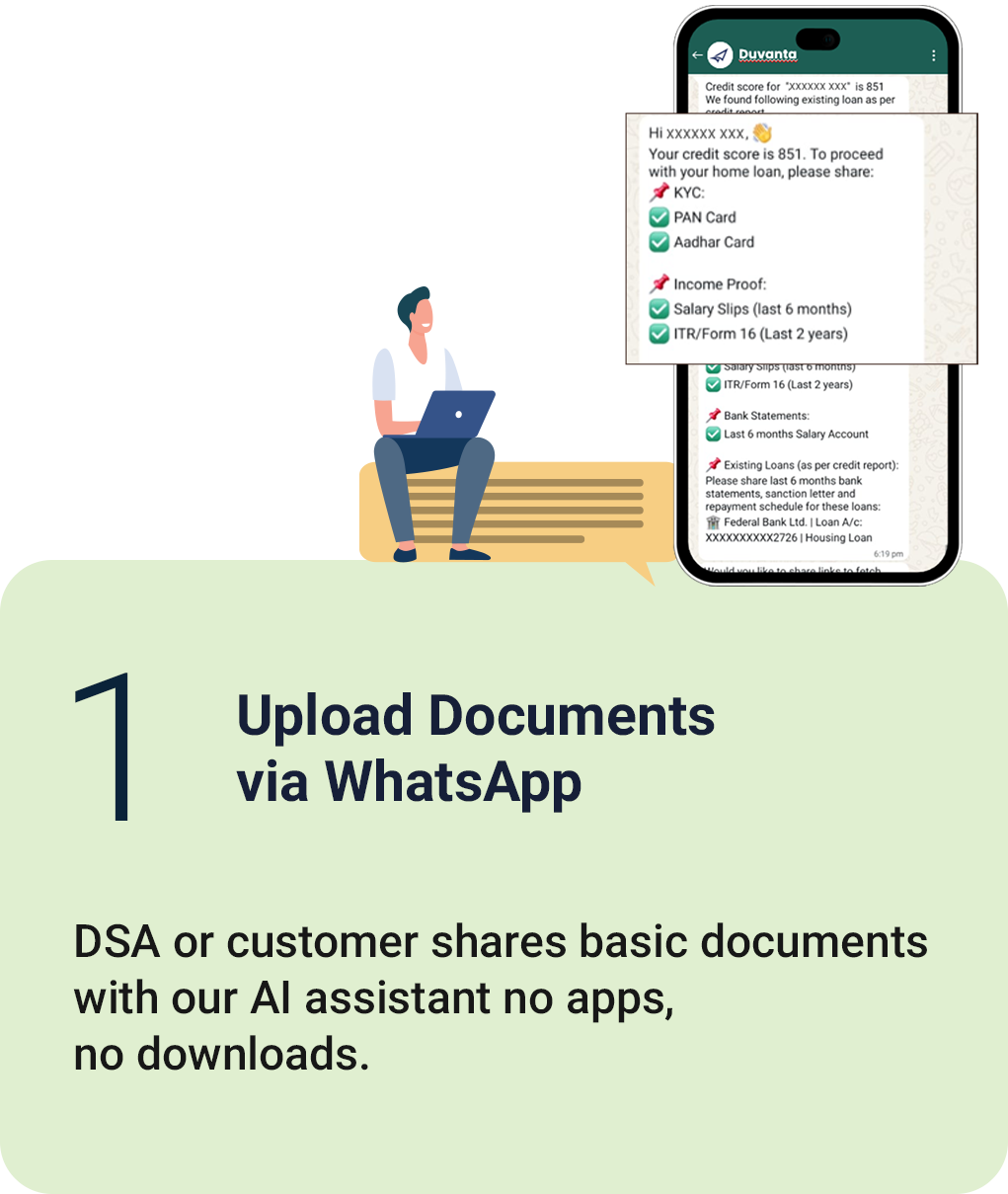

Duvanta automates document collection, eligibility checks, and follow-ups — helping you convert more leads, earn more commissions, and build long-term customer relationships.

Quality files. Faster approvals.

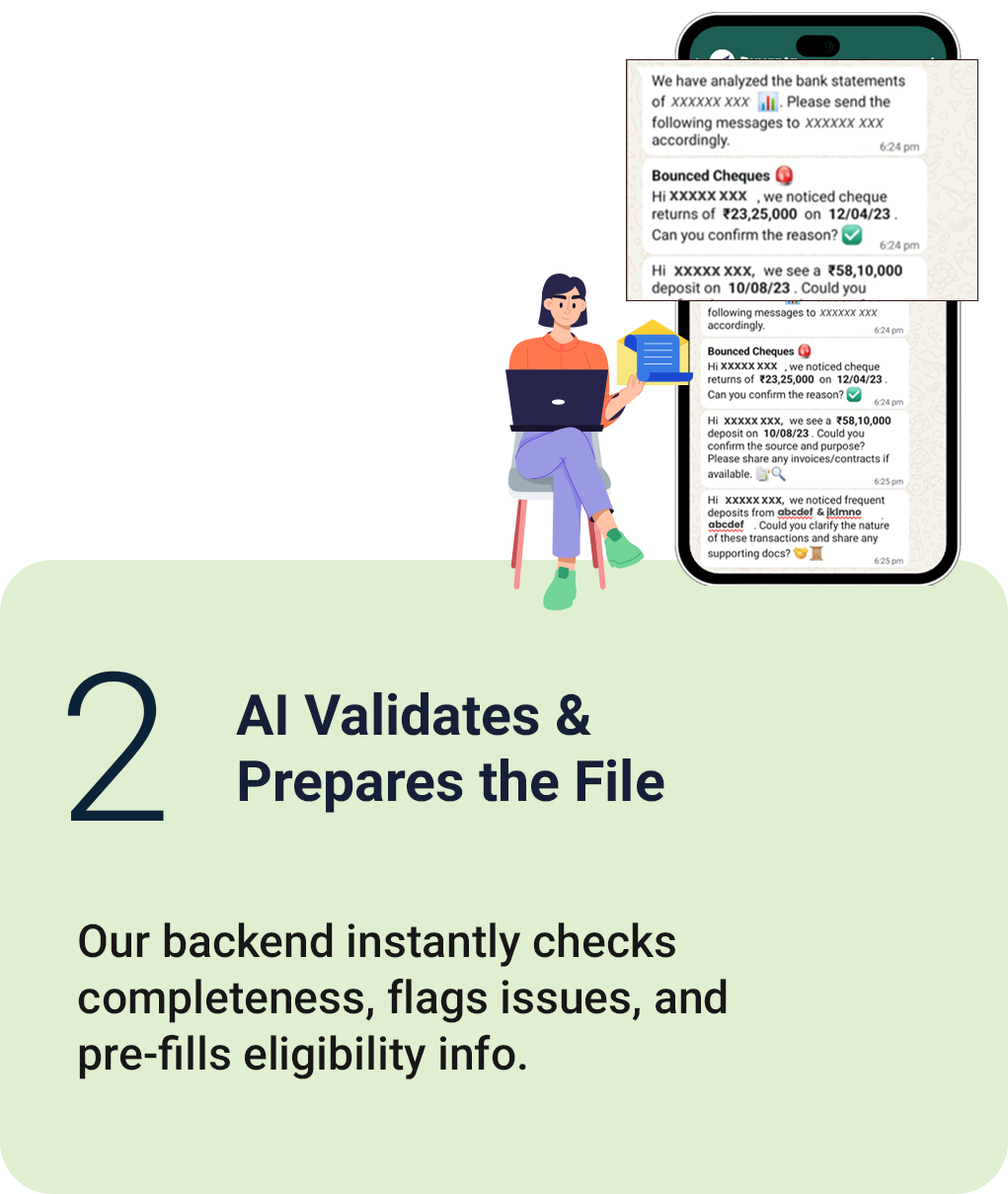

With clean documentation and intelligent workflows, lenders spend less time on incomplete files and more time on approvals — improving TAT, retention, and profitability.

Less paperwork. More clarity.

Borrowers get a WhatsApp-based experience that’s fast, transparent, and frustration-free — improving satisfaction and increasing trust in the entire process.

Stay healthy, stay secure.

Drive worry-free. Save time, close faster.

Duvanta automates document collection, eligibility checks, and follow-ups — helping you convert more leads, earn more commissions, and build long-term customer relationships.

Quality files. Faster approvals.

With clean documentation and intelligent workflows, lenders spend less time on incomplete files and more time on approvals — improving TAT, retention, and profitability.

Less paperwork. More clarity.

Borrowers get a WhatsApp-based experience that’s fast, transparent, and frustration-free — improving satisfaction and increasing trust in the entire process.

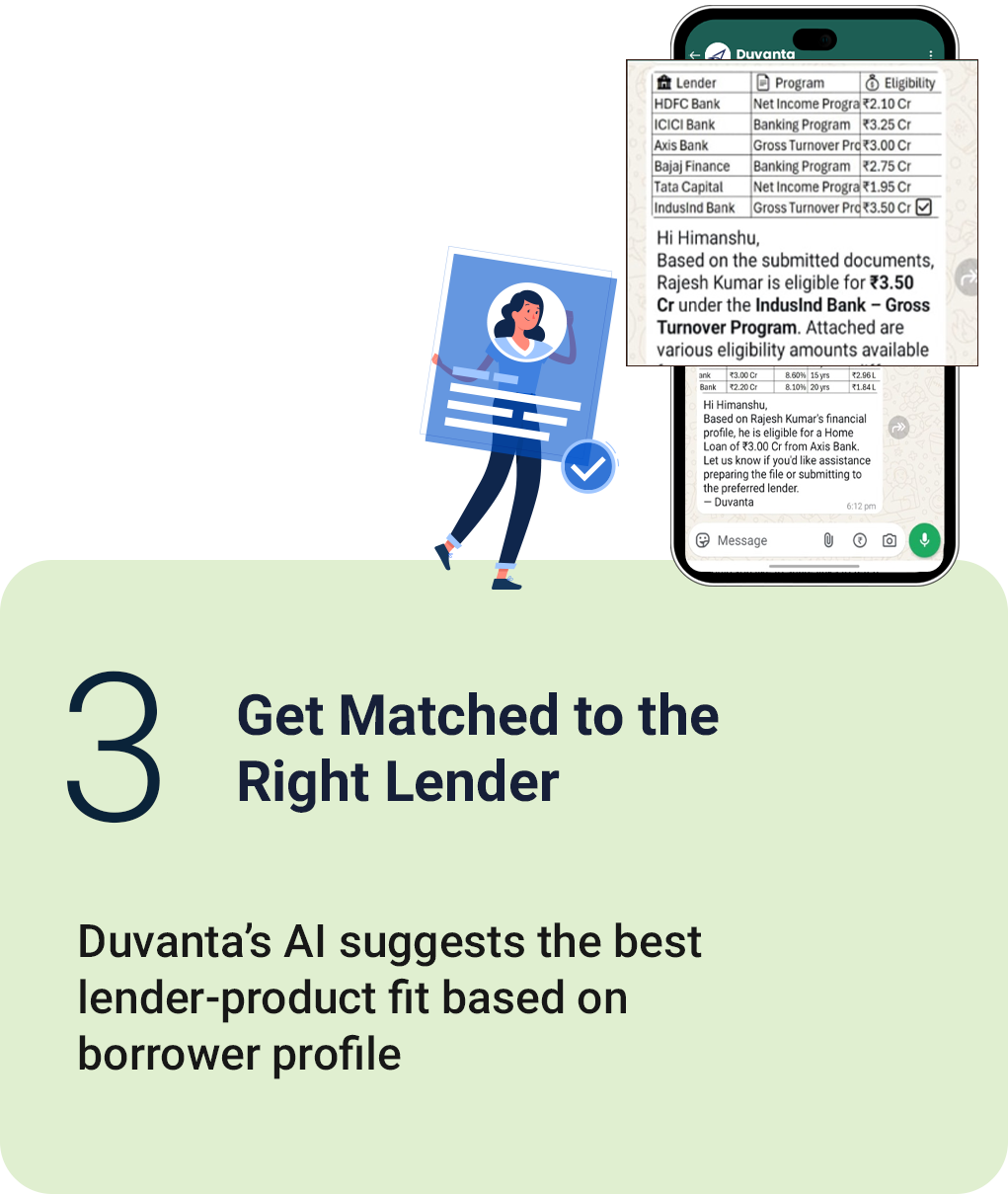

Automated document validation and instant eligibility scoring ensure that files are credit-ready from day one — minimizing manual effort and errors.

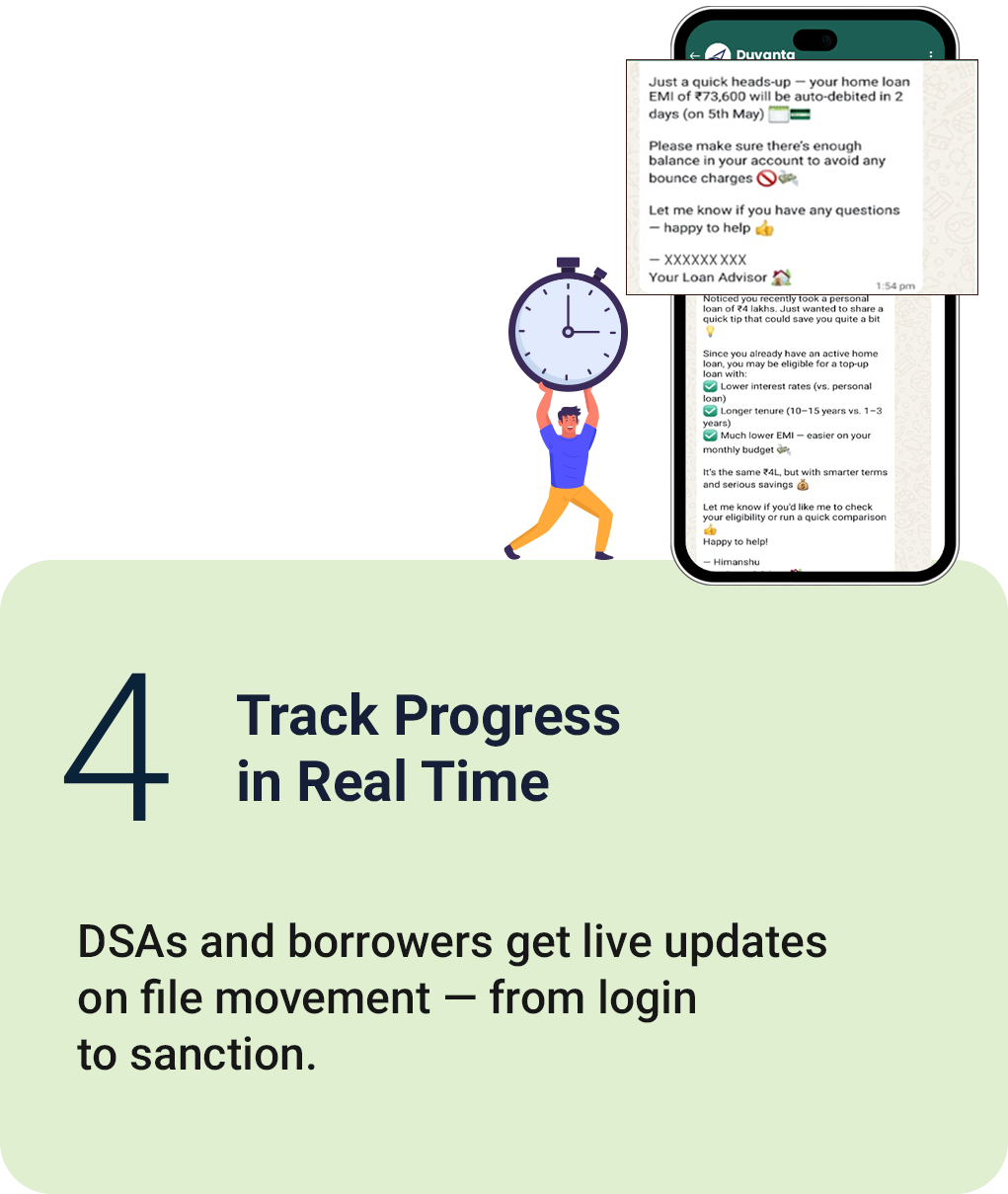

All stakeholders receive instant updates on application progress, eliminating follow-ups and keeping everyone aligned from login to disbursal.

Every lead follows a standardized, intelligent workflow — reducing back-and-forth and enabling quicker credit decisions from lenders.

Built-in lead tracking protects DSA and connector ownership while offering full transparency on payout status and timelines.

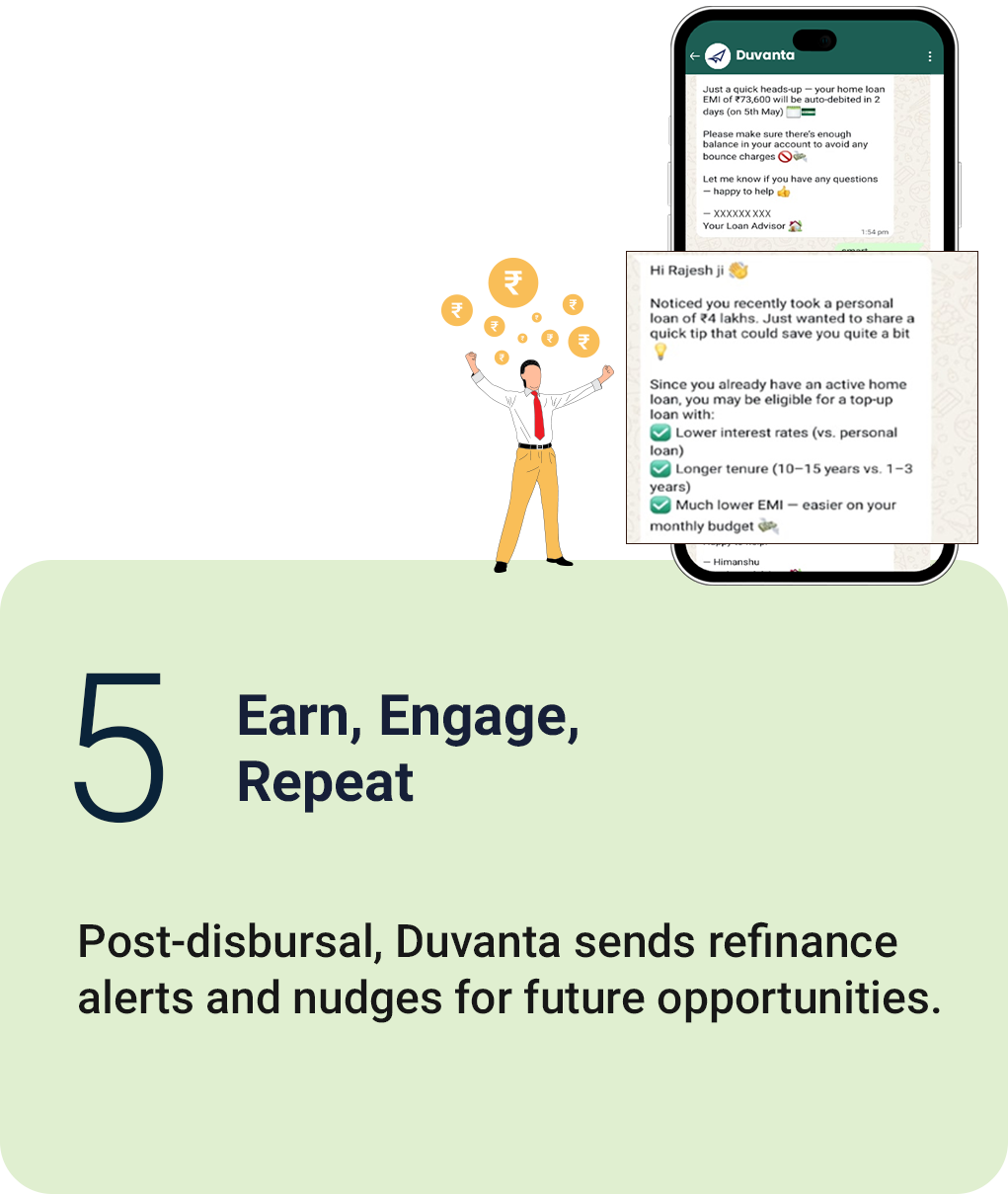

Smart nudges, borrower insights, and re-engagement triggers help DSAs and lenders improve conversion rates and reduce drop-offs across the funnel.

Engage borrowers, DSAs, and connectors where they already are — with a secure, intuitive experience over WhatsApp. No apps, no training required.

Automated document validation and instant eligibility scoring ensure that files are credit-ready from day one — minimizing manual effort and errors.

All stakeholders receive instant updates on application progress, eliminating follow-ups and keeping everyone aligned from login to disbursal.

Every lead follows a standardized, intelligent workflow — reducing back-and-forth and enabling quicker credit decisions from lenders.

Stay healthy, stay secure.

Duvanta automates file preparation and instantly validates eligibility — reducing manual follow-ups, improving file quality, and cutting lead-to-loan time.

All stakeholders stay updated with real-time progress, reducing uncertainty for borrowers and giving DSAs & connectors visibility into deal status.

By ensuring complete, credit-ready files, lenders spend less time on back-and-forth. Borrowers get faster decisions — and confidence in the process.

Our system tracks and protects lead flow, ensuring DSAs and connectors retain ownership and have complete visibility on payouts.

Built-in lead tracking protects DSA and connector ownership while offering full transparency on payout status and timelines.

Smart nudges, borrower insights, and re-engagement triggers help DSAs and lenders improve conversion rates and reduce drop-offs across the funnel.

Engage borrowers, DSAs, and connectors where they already are — with a secure, intuitive experience over WhatsApp. No apps, no training required.

Stay healthy, stay secure.

Duvanta ne mera kaam bahut aasan kar diya. Sab kuch WhatsApp pe ho jaata hai — docs, eligibility, status. Pehle mahine mein 5 cases close karta tha, ab 12-15. Commission bhi 40% tak badh gaya!

Duvanta ka AI assistant file tayar karne mein expert hai. Lead miss hone ka chance hi nahi milta. Jaldi login, jaldi approval — aur customer bhi impress ho jaata hai!

Earlier, I had to follow up five times just to get the right documents. With Duvanta, my files are ready to login on day one. That’s helped me close faster and unlock top-tier commissions from lenders.

What I love about Duvanta is the visibility. I always know where the file is, what’s pending, and when the payout is coming. My approvals have improved, and so has my income — I don’t waste time on dead leads anymore.

Since I started using Duvanta, my business has grown consistently. I’m converting more leads, earning higher payouts, and my borrowers are happier too — they love the fast updates and clear process.

We’re excited about Duvanta’s ability to streamline credit submissions. If the platform continues delivering clean, credit-ready files, we see strong potential to improve our FTNR and TAT metrics.

As adoption scales, we expect Duvanta to meaningfully reduce manual intervention across the sales–credit workflow. That could directly lower our cost-per-loan and boost team productivity.

Duvanta’s structured intake and AI-driven data capture have the potential to significantly improve underwriting quality. We’re optimistic about its impact on risk assessment and borrower segmentation.

We’re onboarding Duvanta with the expectation that it can become a scalable sourcing layer. If the platform continues to deliver quality leads with transparency, it can be a long-term partner in our digital stack

We’re hopeful that Duvanta will help reduce file rejections and shorten disbursal cycles. The early signs are promising, and we’re keen to see its role grow in our origination strategy.

The required property documents for a home loan can vary depending on the purpose of the loan. For instance, the documentation needed to purchase a new house might differ from what’s required for constructing a home. For a detailed list of documents required for a home loan, it’s best to consult with your lender.

The ideal bank for a home loan often depends on the lowest interest rates, as lower rates help reduce the overall interest cost. However, it’s also crucial to consider factors like loan tenure, loan amount, LTV ratio, processing fees, and the speed of loan approval. Instead of individually visiting each lender’s website, you can simplify your search by using online financial marketplaces (like Duvnta .com) to compare home loan rates and features from various banks and HFCs.

No, home loans do not cover the entire property value. The Reserve Bank of India (RBI) has set Loan-to-Value (LTV) ratio limits. For loans up to Rs 30 lakh, the LTV ratio can be up to 90%. For loans between Rs 30 lakh and Rs 75 lakh, it’s capped at 80%, and for loans above Rs 75 lakh, the LTV ratio is limited to 75%. Borrowers must cover the remaining amount through a down payment.

The maximum home loan amount is often determined by the lender using methods like the Multiplier Method or the EMI/NMI Ratio. These methods consider your income and existing financial obligations. Some lenders also combine these methods to assess your eligibility.

Lenders assess your ability to repay by considering your total EMI obligations, including the proposed home loan EMI, which should ideally be within 50-60% of your monthly income. Online EMI calculators can help you estimate the optimal loan amount and tenure based on your repayment capacity.

Obtaining a home loan with a low credit score is challenging, as different lenders have varying credit risk policies. It's advisable to use online platforms to compare home loan rates and terms from multiple lenders, even with a poor credit score.

Lenders generally prefer applicants with a credit score of 750 or above, as it indicates responsible credit behavior and lowers credit risk. A high credit score can also qualify you for better interest rates. Regularly checking your credit score is recommended.

The EMI for a Rs. 20 lakh home loan depends on the interest rate and tenure. For example, at an 8.50% interest rate over 20 years, the EMI would be Rs. 17,356. You can use an EMI calculator to determine EMIs for different rates and tenures.

Your spouse or close family members like parents, siblings, or children can co-sign a home loan with you. Additionally, all co-owners of the property must be co-applicants.

For floating-rate home loans, lenders do not charge prepayment penalties as per RBI regulations. However, fixed-rate home loans may incur prepayment fees.

A home loan balance transfer allows borrowers to switch their existing loan to another lender with lower interest rates or better terms. This option is beneficial for those who initially secured a loan at a higher rate and now qualify for a lower rate.

Yes, you can take a second home loan if the lender is satisfied with your repayment capacity, credit profile, and the details of the second property.

Home loan approval typically takes 1 to 2 weeks but can vary based on the lender’s process, your credit profile, and the property details.

A fixed-rate home loan has a constant interest rate throughout the loan tenure, protecting you from rate increases but also preventing you from benefiting if rates drop. A floating-rate loan’s interest rate fluctuates with market conditions, often offering lower initial rates but with potential changes over time.

Yes, you can prepay your home loan. For floating-rate loans, no prepayment charges apply. However, fixed-rate loans may incur fees, typically 2-4% of the prepaid amount.

Yes, the principal repayment qualifies for deductions under Section 80C of the Income Tax Act, and the interest payment qualifies under Section 24(b).

Yes, most lenders allow borrowers to switch from a fixed-rate to a floating-rate loan (or vice versa) by paying a conversion fee.

Under the Pradhan Mantri Awas Yojana-Gramin (PMAY-G) scheme, beneficiaries can avail a maximum home loan amount of up to Rs 70,000.

Key documents include identity and address proof, income statements, bank statements, credit reports, property documents, and proof of employer address. Requirements may vary across lenders.

Yes, applying with a co-applicant like a spouse or family member can enhance your loan eligibility by combining incomes.

Yes, having a stable job with a reputable employer and substantial work experience increases your chances of loan approval. Self-employed individuals can still secure home loans with sufficient income proof.

Duvanta offers expert guidance and impartial advice, helping you navigate the home loan process to find the best loan without pressuring you to make quick decisions.

Where Mortgage Meets Intelligence — Smarter Loans, Happier Customers, Stronger Growth

Copyright © 2025 Duvanta Solutions Pvt. Ltd. All rights reserved.

WhatsApp us